News

E&S Revenue Keeps Rising in Tough Market

The excess and surplus lines market continues to attract more business six years into a period of sustained rate hikes for many lines of commercial property/casualty insurance coverage.

Nearly all the wholesalers, managing general agents and underwriting managers in Business Insurance’s rankings reported double-digit premium volume and revenue increases in 2023 (see charts here). While acquisitions drove some of the growth, overall premiums in the E&S sector continued to rise, according to state reports (see chart here).

The top 10 wholesalers collectively reported $95.48 billion in written premium in 2023, a 26% increase over the 2022 top 10. Among MGAs, underwriting managers and Lloyd’s coverholders, the 2023 top 10 reported $25.83 billion in premium, up a more modest 5.6%, but the composition of the group changed more markedly.

The largest companies in the sector remain the same. The largest overall intermediary in the specialty sector remained CRC Group, a unit of TIH Insurance Holdings LLC, though Amwins Group Inc., which reported about 20% growth last year, narrowed the gap between first and second to less than $400 million in premium volume, and Amwins continued to report the most property/casualty premium. Ryan Specialty LLC was again the third-largest specialty intermediary, with all the top three larger than the other companies in the top 10 by some distance.

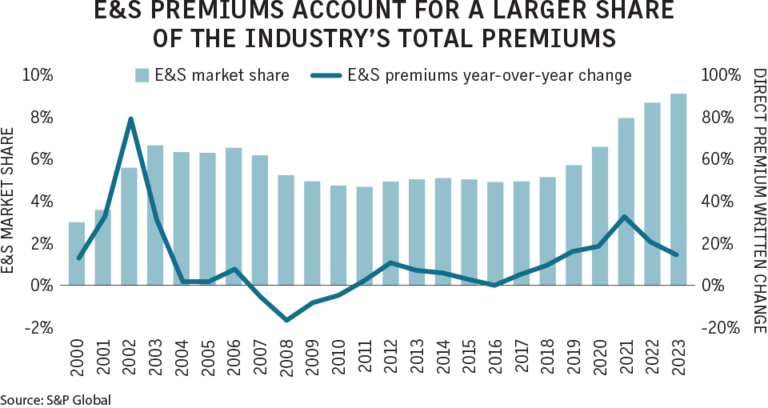

While the sector continued to expand, the pace of growth slowed, according to a June report by S&P Global Market Intelligence. Direct premium rose 14.5% in 2023, which was down from 20.1% in 2022. However, the E&S market now makes up 9.2% of U.S. total direct premiums written, up from 5.2% at the beginning of the market hardening in 2018, the report stated.

Property lines saw a 41% surge in direct premium in 2023 compared with the prior year, S&P reported. Rising reinsurance costs and limited appetite among admitted insurers to write business in catastrophe-prone states accounted for the increase, S&P said.

Overall liability lines accounted for 52.5% of E&S premium, property accounted for 31.7% and commercial auto 5.4%.